Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

a16z Visual: AI Cost Halving, Usage Doubling, U.S. 30-Somethings Enter the 'Adulthood Delay' Era

Original Title: Charts of the Week: DExit . . . real or feigned?

Original Source: a16z New Media

Original Translation: DeepTech TechFlow

DeepTech Summary: This week's a16z Chart Report covers four topics, each worthy of its own article: AI cost declines triggering the Jevons effect, the true scale of Big Tech capital expenditure, Kalshi prediction markets outperforming expert forecasters, and the comprehensive delay of American 30-something milestones. With solid data sources and a calm, restrained perspective, it is a high-quality reference for understanding the current intersection of technology and macro trends.

DExit... A Real Trend or an Illusion?

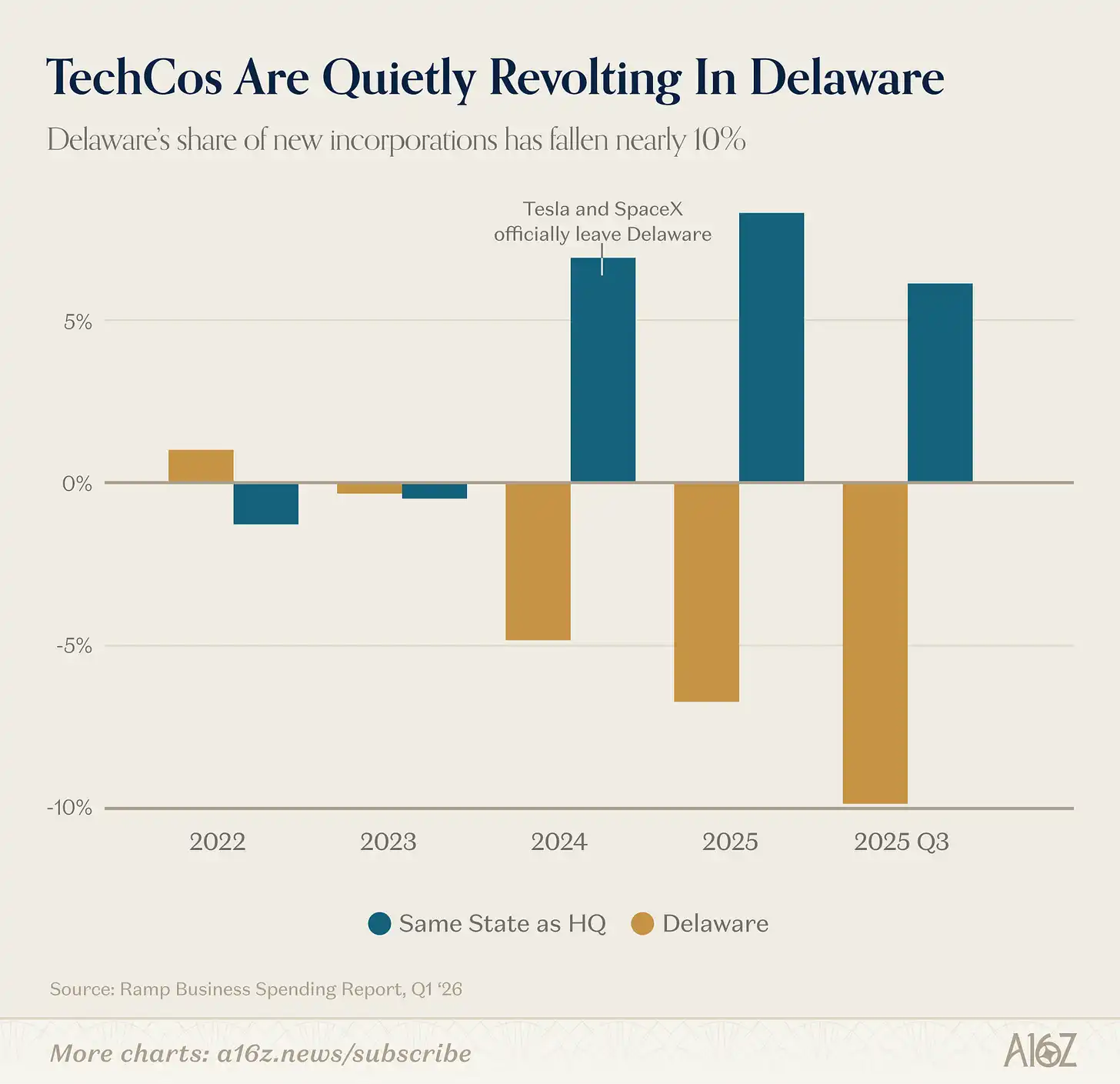

Delaware remains the top choice for U.S. company incorporation, but this position is quietly slipping:

According to Ramp's data, Delaware's share in new company registrations has been declining since 2023, with a roughly 10% drop in the third quarter of 2025.

History does not merely repeat itself, but it often rhymes... maybe.

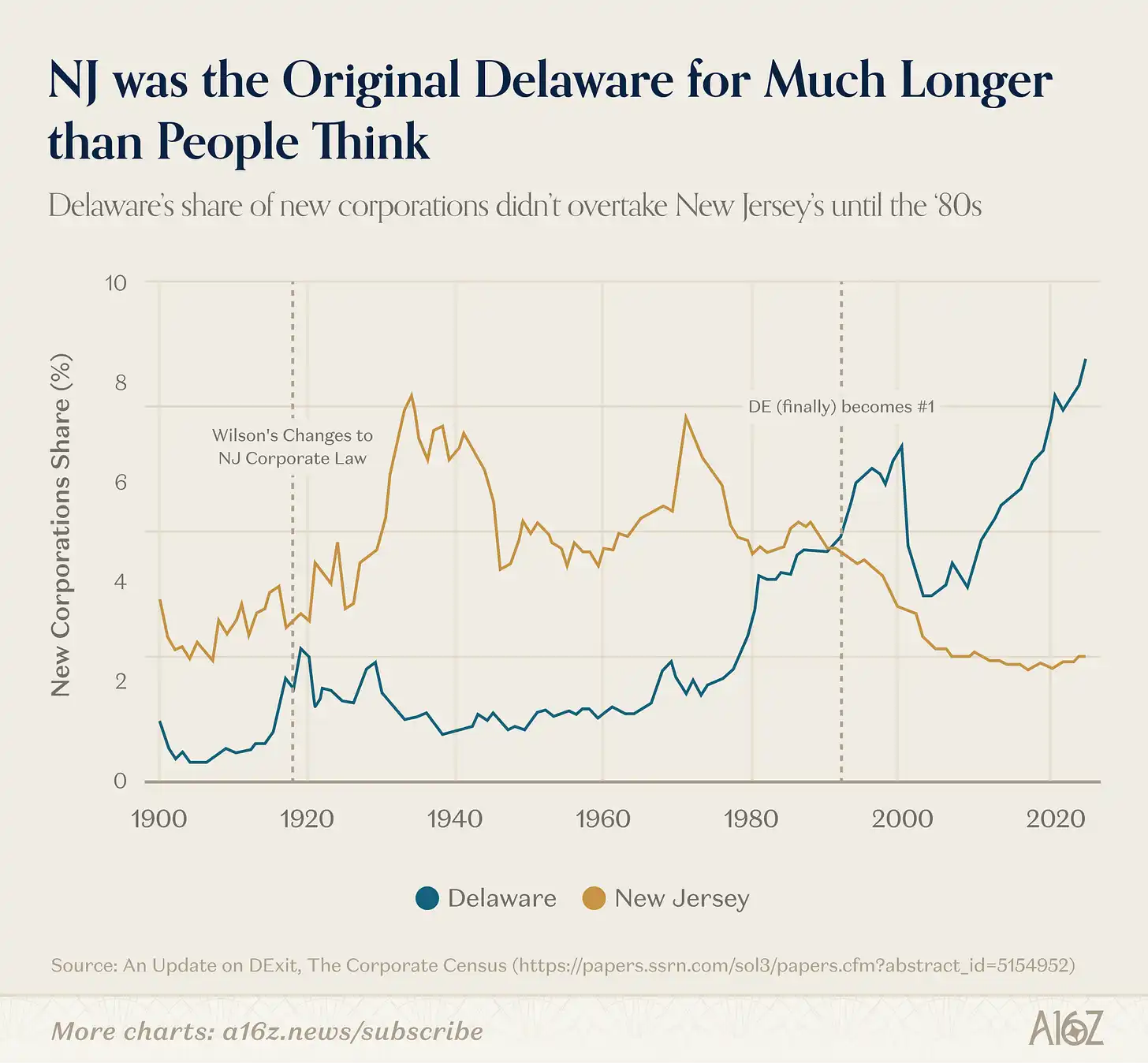

Delaware has not always been the mecca of corporate registration.

About a century ago, Delaware replaced New Jersey—the original "mother of trusts"—as the preferred destination for company registration. New Jersey lost its edge because then-Governor Woodrow Wilson sought to curb "corporate abuses," significantly deteriorating New Jersey's business environment. Delaware's corporate law was modeled after the pre-Wilson era New Jersey laws and was naturally welcoming to fleeing enterprises. Subsequently, by joining the Delaware Chancery Court, it spent nearly 100 years building a reputation as a mature and impartial venue for resolving corporate and investor disputes.

However, something that took a century to build started to shake in just a few years. Regardless of right or wrong, the Delaware Chancery Court has taken a more lenient stance on shareholder litigation in recent years (especially in several high-profile cases, including but not limited to Tesla), prompting companies to genuinely move their registrations elsewhere. Good night, and good luck, Delaware.

This is at least the mainstream narrative, but other data paints a more complex picture.

First, even the foundational myth of Delaware is not entirely accurate.

It wasn't until the 1980s (about 60 years into Governor du Pont's reign) that Delaware truly pulled ahead of New Jersey to become the top state for business entities in the U.S.:

New Jersey's dominance lasted far longer than the mainstream narrative describes. Delaware's eventual leap forward was likely catalyzed by passing a series of laws related to directorial responsibility that made it especially attractive to public companies, along with network effects that continually reinforced themselves, generating its own momentum.

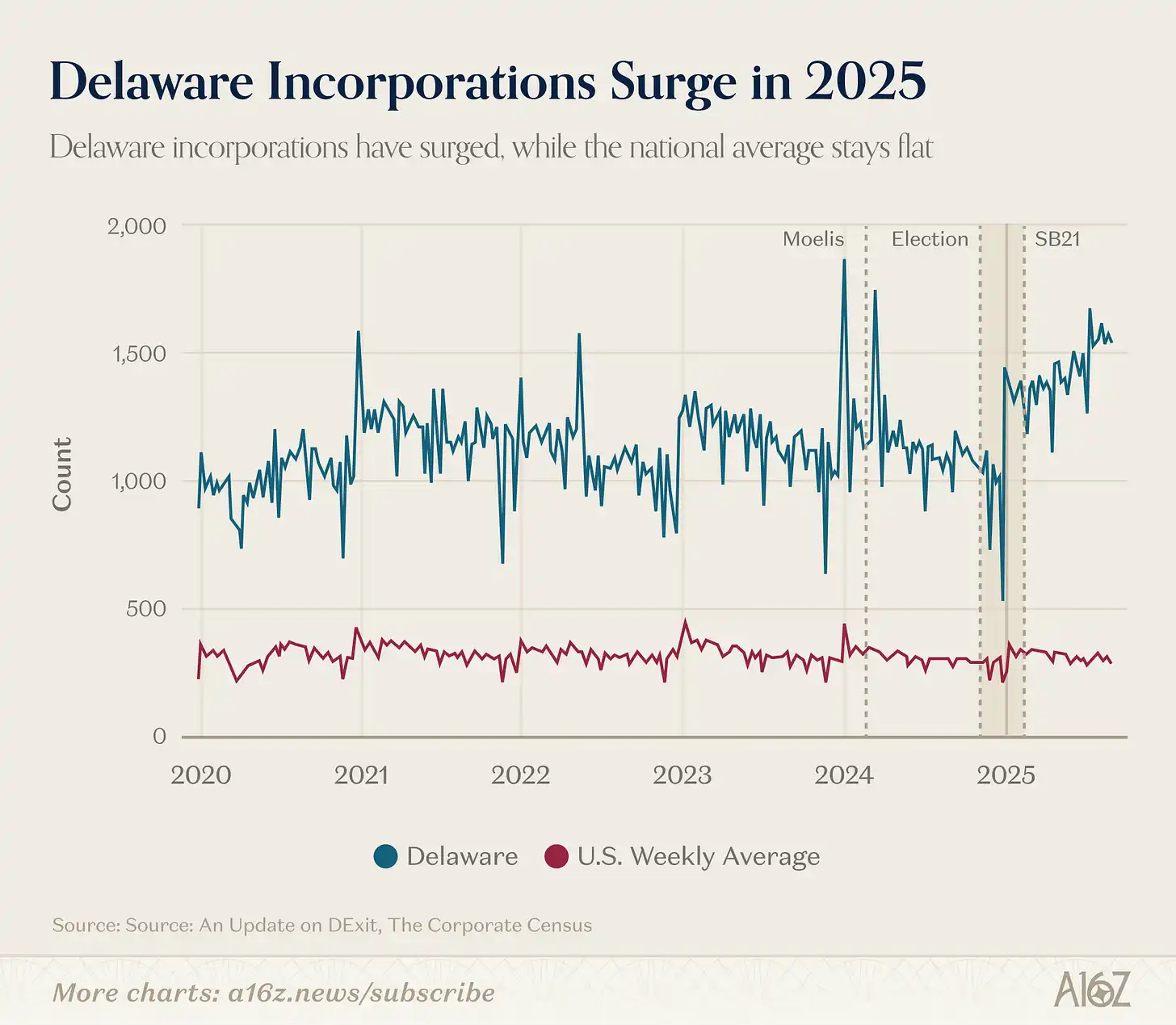

Second, regardless of what's happening with high-profile public companies (and companies in the Ramp data), Delaware as a whole still seems to be doing well, and more than that:

According to data released by the Harvard Law School Forum on Corporate Governance, from the end of 2024 to 2025, Delaware's share of total U.S. businesses actually saw a significant increase.

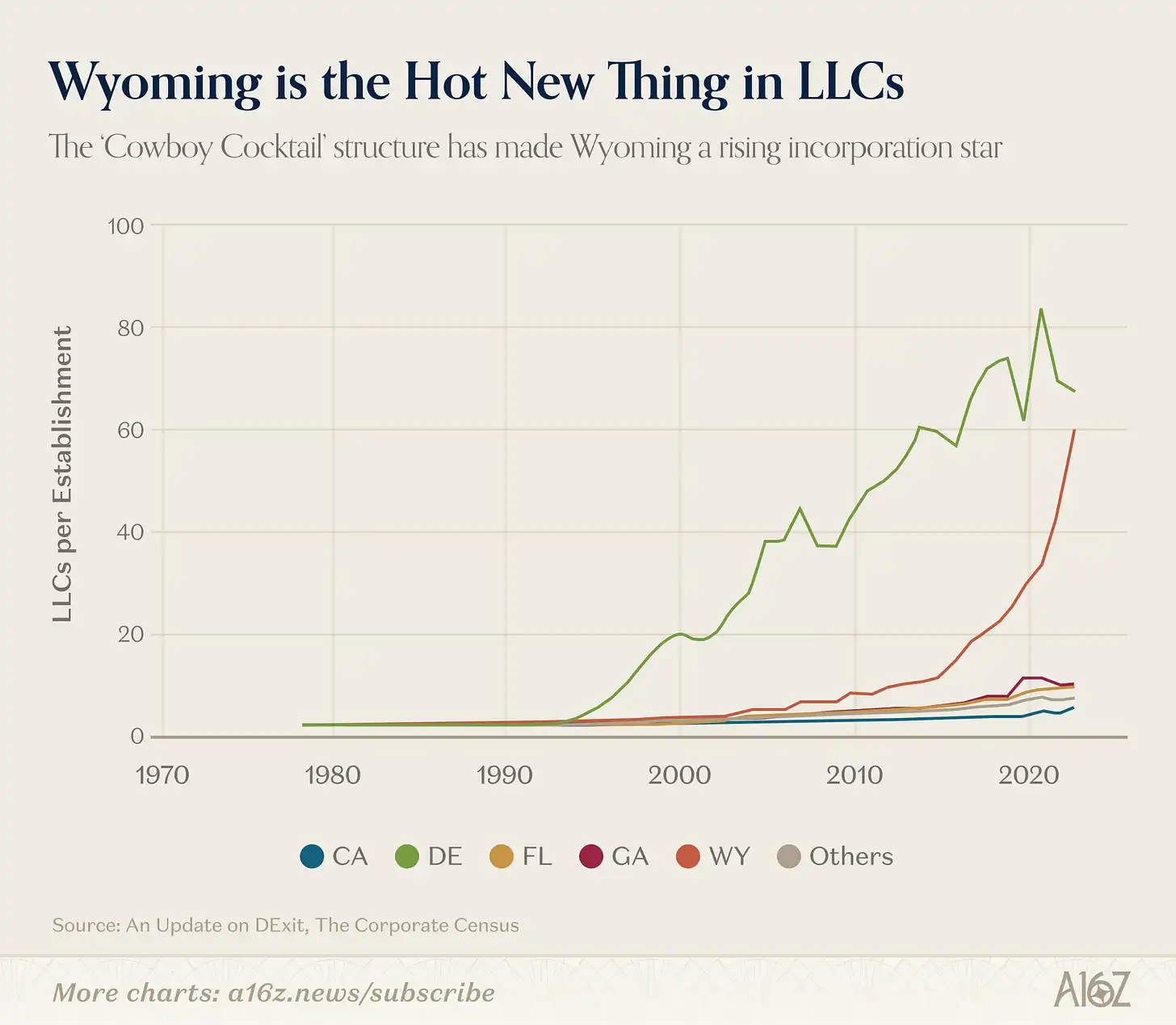

In fact, if you're looking for a clear "DExit" case, it's probably this, and it has nothing to do with Tesla but instead involves a specific corporate form:

LLCs in Wyoming started to skyrocket around 2015.

Why? This likely has to do with specific asset protection and privacy provisions in Wyoming's LLC laws, which the state itself markets as a "Cowboy Cocktail" of company structures.

The key takeaway here is not to say that DExit isn't happening (because at least some data suggests that it is happening — even if only a few high-profile companies leaving carries weight), but the reality is certainly more complex than what the mainstream narrative presents.

The reality is that Delaware still enjoys the advantage of being the default option, not to mention all the network effects tied to it that are hard to disrupt.

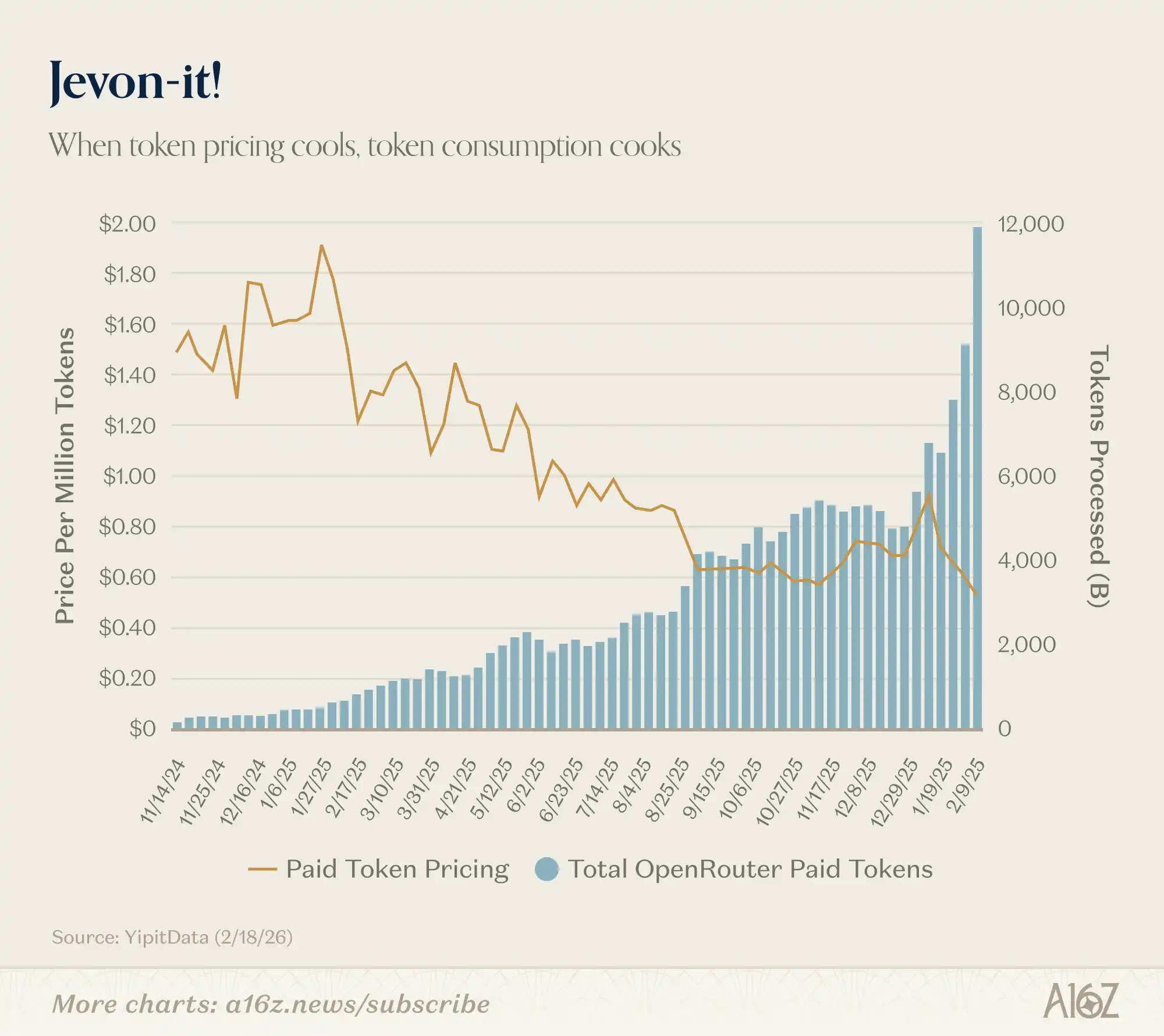

We've posted earlier versions of this chart, but with more data, the effect is even more striking.

Token Costs Down, Token Consumption Up:

Since the beginning of this year, the price of paid tokens has dropped from about $0.90 per million tokens to $0.50, while the number of tokens processed has almost doubled, increasing from about 6,000 to 12,000.

This is a typical Jevons Paradox. The cheaper AI gets, the more AI we use. Delightful.

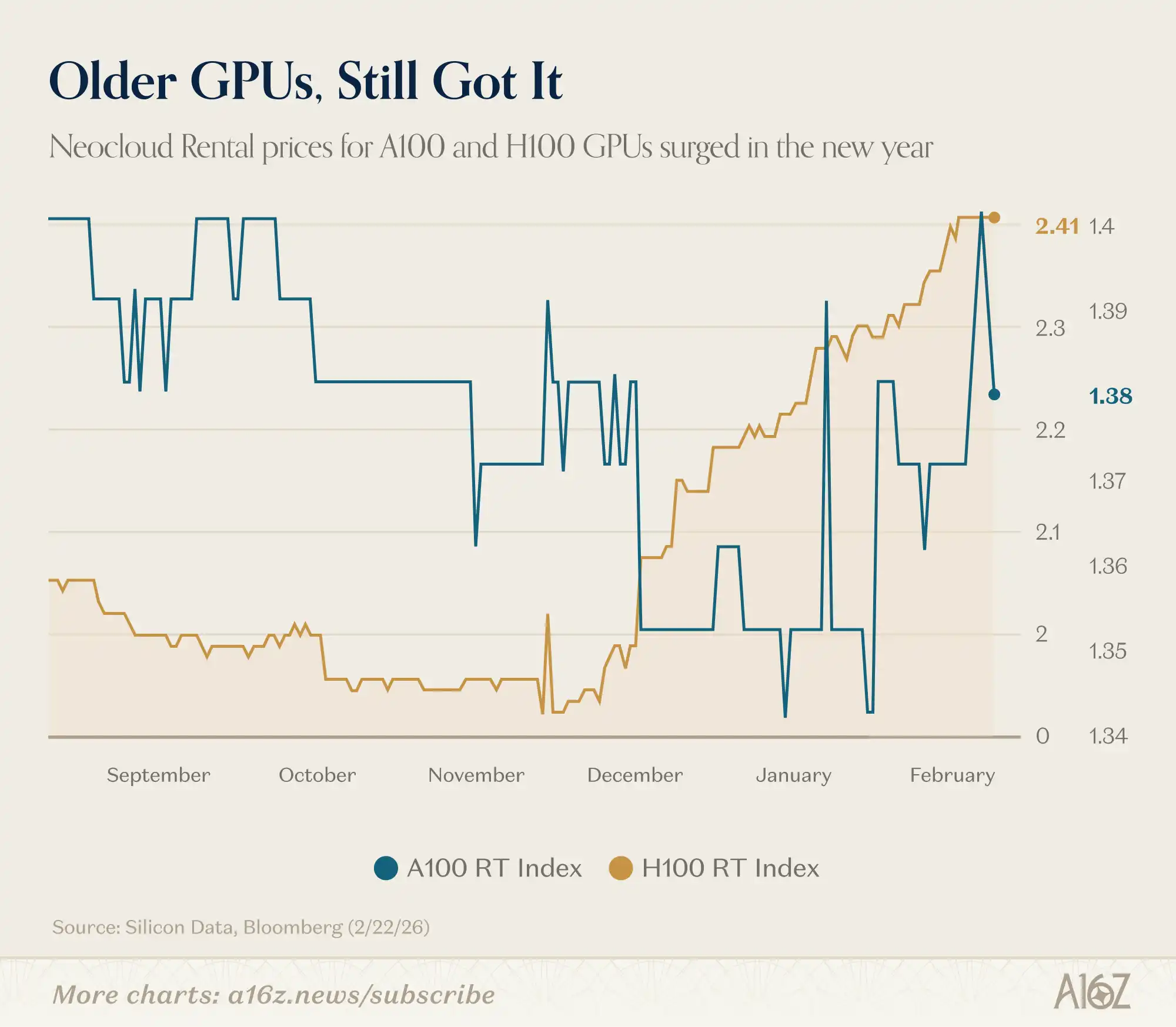

Remember when someone said that once newer and better GPUs are released, no one would want the old ones anymore?

Well, it seems that's not quite the case:

According to Silicon Data, the rental prices of NVIDIA H100 and A100 have both increased this year.

There are no signs in the market of an oversupply of mining power. It seems like the surface of the existing demand has not even been scratched yet.

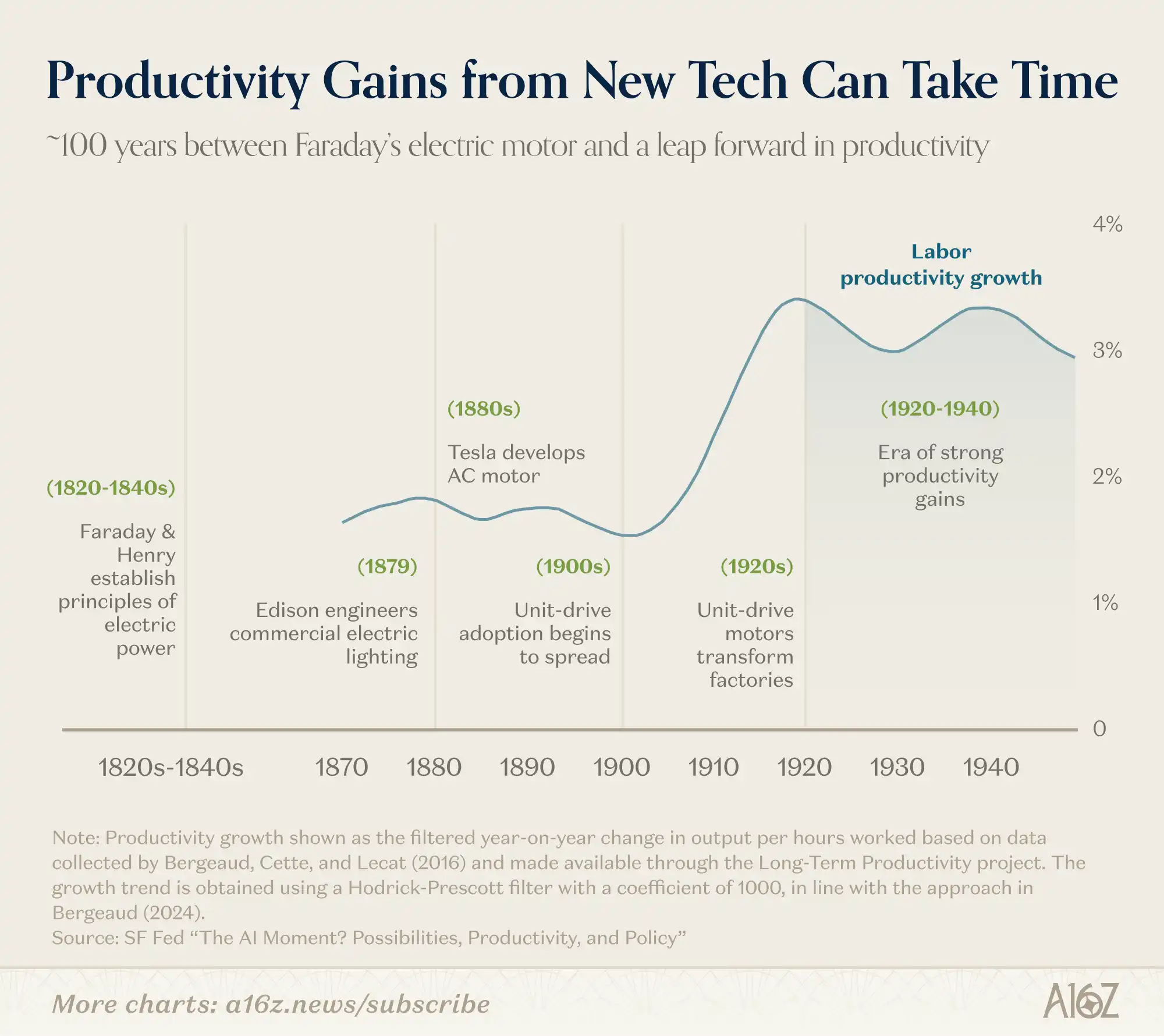

While this comparison is not perfect, if history is any guide, it may take some time to truly "see" what the AI-driven "economy" will look like:

From Faraday and Henry's initial discussions of electricity to the real surge in industrial productivity in the first half of the 20th century, it took about 100 years.

Since the 1820s, the pace of technological iteration has indeed accelerated, but the variables involved in a platform-level shift are still extremely numerous.

Roy Amara had a famous saying: "We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten years."

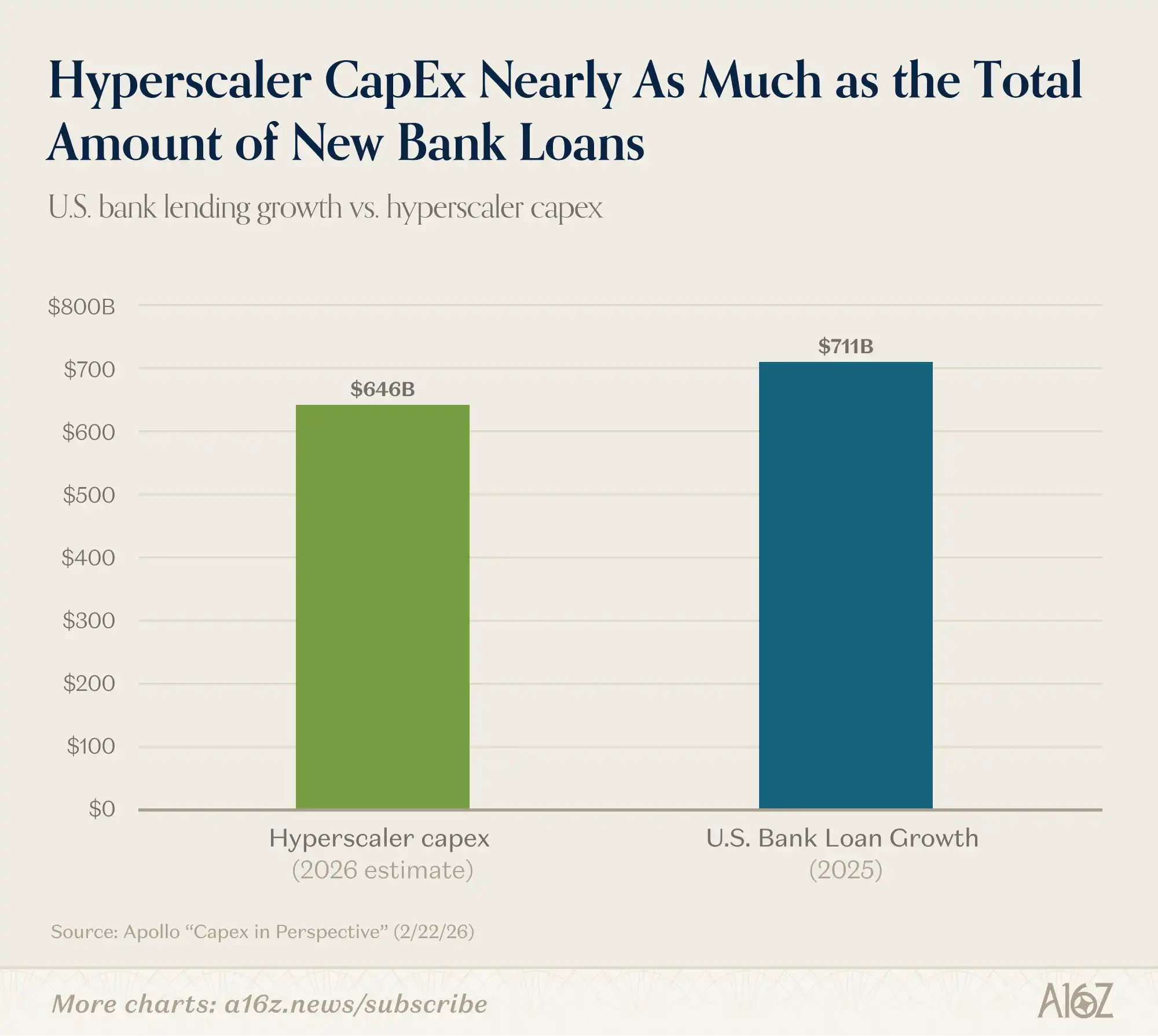

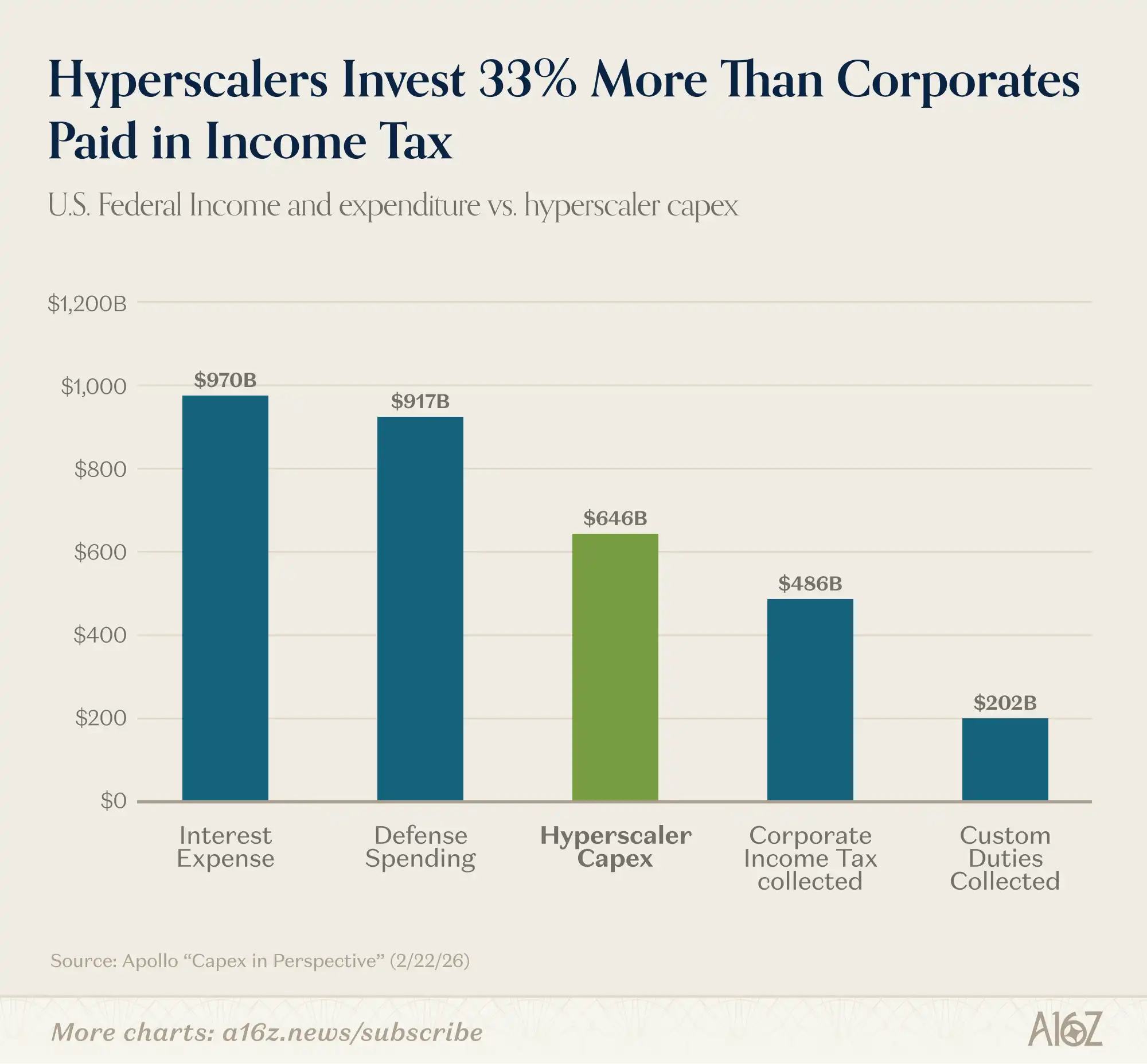

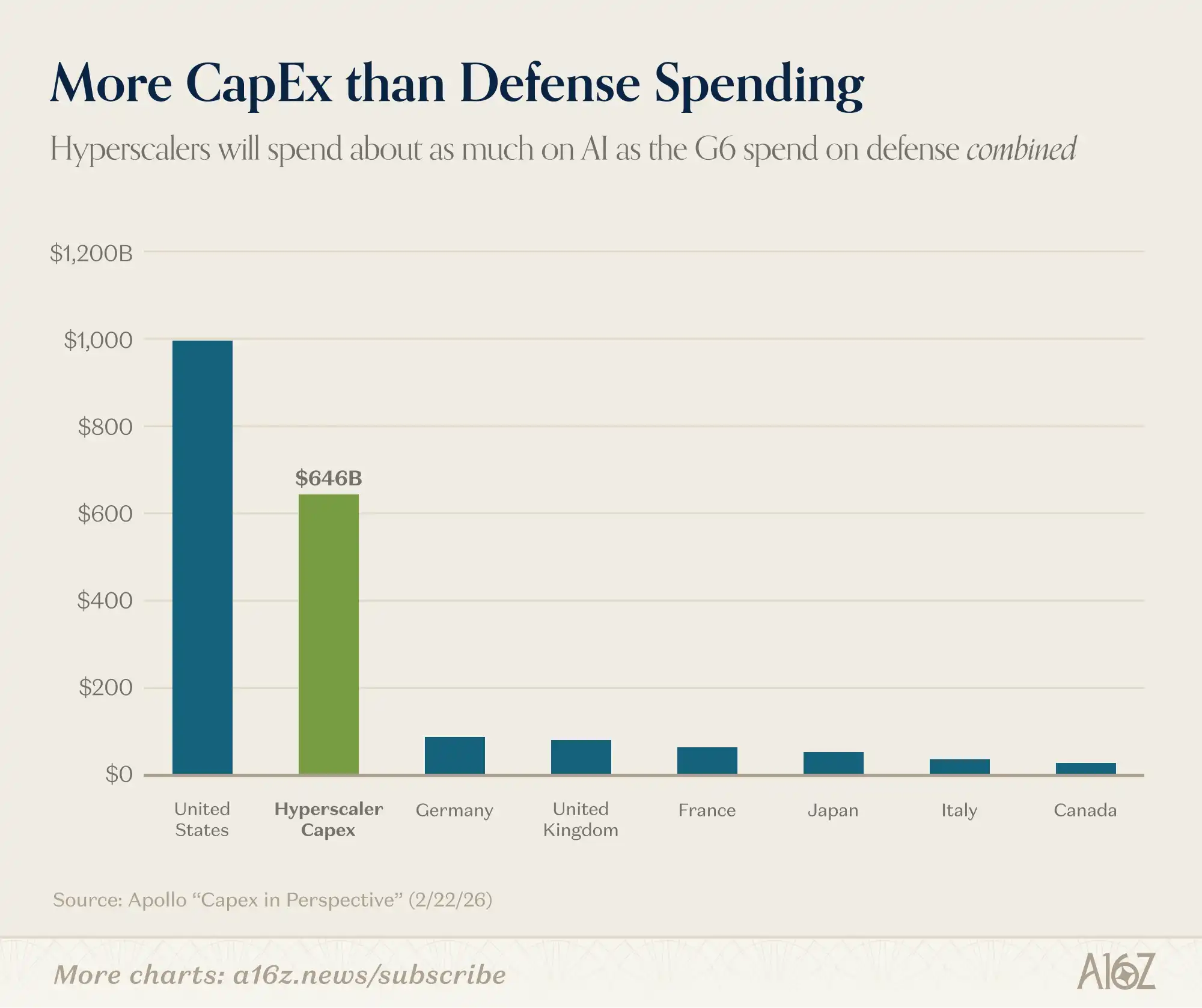

Capital Expenditure, Plotted on a Graph

Look at this set of timeless data: AI capital expenditure is substantial.

Consider the following comparisons:

AI capital expenditure in 2026 is projected to be nearly equivalent to the total net new loans of all U.S. banks in 2025:

Capital expenditure is around 33% higher than the total corporate income tax revenue in the U.S. and about three times the total tariff amount:

Capital expenditure is about six times the total military budget of any non-U.S. G7 member:

So, yes, the scale of capital expenditure is indeed substantial.

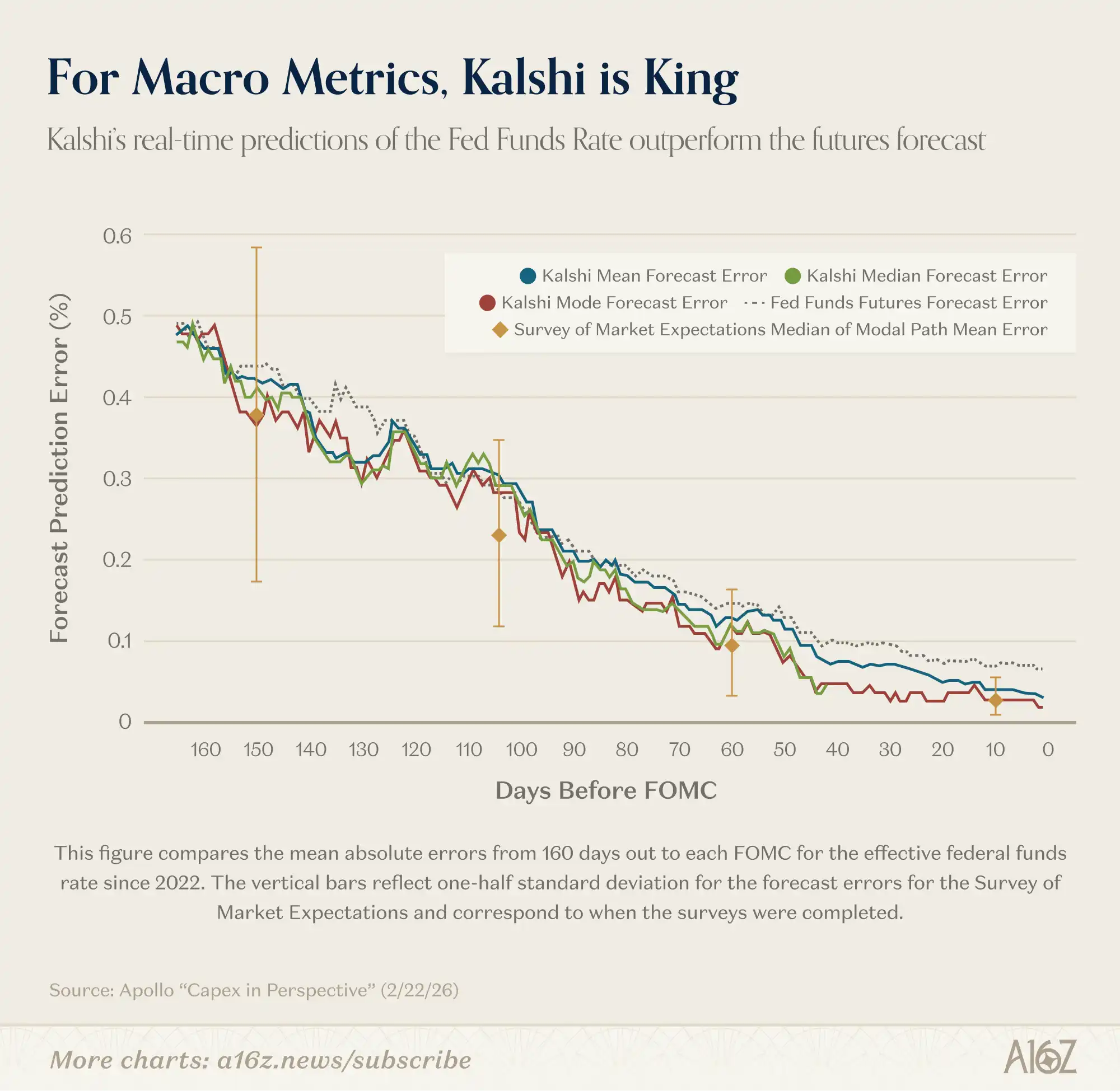

Kalshi Makes Inroads in Macro Forecasting

A Fed researcher believes prediction markets are quite good.

At least on one measure, Kalshi's performance in forecasting the federal funds rate has surpassed that of professional forecasters:

For the 150-day-ahead (i.e., post 3 FOMC meetings) federal funds rate forecast, Kalshi's mean absolute error is very close to that of professional forecasters. But unlike surveys that provide a modal path snapshot only every six weeks, Kalshi provides continuously updated full probability distributions... We find that Kalshi's median and mode forecasts are perfectly accurate at the forecast time of day prior to the FOMC meeting, a statistically significant improvement over federal funds futures forecasts.

In other words, while all forecasters start about the same, Kalshi's continuously updated forecasts optimize over time, ultimately achieving a perfect forecast record the day before the rate is announced. Additionally, Kalshi's performance surpasses that of the futures market forecasts.

Kalshi's advantage extends beyond the federal funds rate. As Fed researchers point out, since macroeconomic indicators like inflation, growth, and unemployment lack other options markets, Kalshi is the only place to provide a "high-frequency, continuously updated, richly distributed 'benchmark' where 'the crowd' opines on where these economic indicators are headed."

That sounds pretty important.

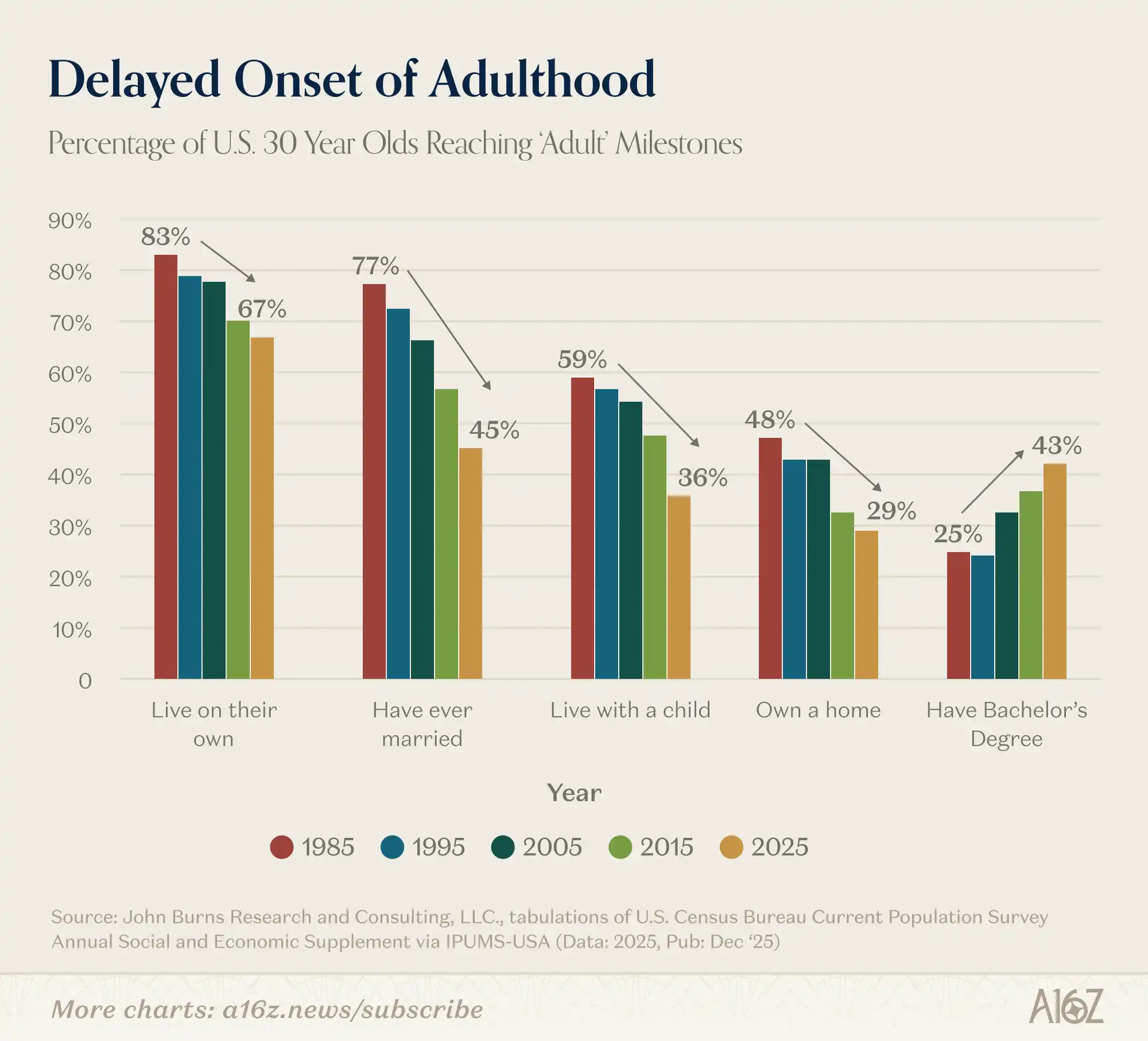

The Age of Delayed Adulthood

Here is a thought-provoking chart with a (small) commentary:

The share of the 30-year-olds achieving major life milestones has been on a steep decline, at least since the 1980s.

Among 30-year-olds, fewer and fewer are:

Living independently;

Ever married;

Living with children;

Owning their own homes.

The only exception is college enrollment — the share of 30-year-olds with a bachelor's degree has nearly doubled since 1995.

So, is going to college worth it?

Milestone? Feels more like a neck-grinding millstone, doesn't it?!

Maybe yes, maybe no, but the "buyer's remorse" emotion seems to be hanging in the air.

You may also like

Consumer-grade Crypto Global Survey: Users, Revenue, and Track Distribution

Prediction Markets Under Bias

Stolen: $290 million, Three Parties Refusing to Acknowledge, Who Should Foot the Bill for the KelpDAO Incident Resolution?

ASTEROID Pumped 10,000x in Three Days, Is Meme Season Back on Ethereum?

ChainCatcher Hong Kong Themed Forum Highlights: Decoding the Growth Engine Under the Integration of Crypto Assets and Smart Economy

Why can this institution still grow by 150% when the scale of leading crypto VCs has shrunk significantly?

Anthropic's $1 trillion, compared to DeepSeek's $100 billion

Geopolitical Risk Persists, Is Bitcoin Becoming a Key Barometer?

Annualized 11.5%, Wall Street Buzzing: Is MicroStrategy's STRC Bitcoin's Savior or Destroyer?

An Obscure Open Source AI Tool Alerted on Kelp DAO's $292 million Bug 12 Days Ago

Mixin has launched USTD-margined perpetual contracts, bringing derivative trading into the chat scene.

The privacy-focused crypto wallet Mixin announced today the launch of its U-based perpetual contract (a derivative priced in USDT). Unlike traditional exchanges, Mixin has taken a new approach by "liberating" derivative trading from isolated matching engines and embedding it into the instant messaging environment.

Users can directly open positions within the app with leverage of up to 200x, while sharing positions, discussing strategies, and copy trading within private communities. Trading, social interaction, and asset management are integrated into the same interface.

Based on its non-custodial architecture, Mixin has eliminated friction from the traditional onboarding process, allowing users to participate in perpetual contract trading without identity verification.

The trading process has been streamlined into five steps:

· Choose the trading asset

· Select long or short

· Input position size and leverage

· Confirm order details

· Confirm and open the position

The interface provides real-time visualization of price, position, and profit and loss (PnL), allowing users to complete trades without switching between multiple modules.

Mixin has directly integrated social features into the derivative trading environment. Users can create private trading communities and interact around real-time positions:

· End-to-end encrypted private groups supporting up to 1024 members

· End-to-end encrypted voice communication

· One-click position sharing

· One-click trade copying

On the execution side, Mixin aggregates liquidity from multiple sources and accesses decentralized protocol and external market liquidity through a unified trading interface.

By combining social interaction with trade execution, Mixin enables users to collaborate, share, and execute trading strategies instantly within the same environment.

Mixin has also introduced a referral incentive system based on trading behavior:

· Users can join with an invite code

· Up to 60% of trading fees as referral rewards

· Incentive mechanism designed for long-term, sustainable earnings

This model aims to drive user-driven network expansion and organic growth.

Mixin's derivative transactions are built on top of its existing self-custody wallet infrastructure, with core features including:

· Separation of transaction account and asset storage

· User full control over assets

· Platform does not custody user funds

· Built-in privacy mechanisms to reduce data exposure

The system aims to strike a balance between transaction efficiency, asset security, and privacy protection.

Against the background of perpetual contracts becoming a mainstream trading tool, Mixin is exploring a different development direction by lowering barriers, enhancing social and privacy attributes.

The platform does not only view transactions as execution actions but positions them as a networked activity: transactions have social attributes, strategies can be shared, and relationships between individuals also become part of the financial system.

Mixin's design is based on a user-initiated, user-controlled model. The platform neither custodies assets nor executes transactions on behalf of users.

This model aligns with a statement issued by the U.S. Securities and Exchange Commission (SEC) on April 13, 2026, titled "Staff Statement on Whether Partial User Interface Used in Preparing Cryptocurrency Securities Transactions May Require Broker-Dealer Registration."

The statement indicates that, under the premise where transactions are entirely initiated and controlled by users, non-custodial service providers that offer neutral interfaces may not need to register as broker-dealers or exchanges.

Mixin is a decentralized, self-custodial privacy wallet designed to provide secure and efficient digital asset management services.

Its core capabilities include:

· Aggregation: integrating multi-chain assets and routing between different transaction paths to simplify user operations

· High liquidity access: connecting to various liquidity sources, including decentralized protocols and external markets

· Decentralization: achieving full user control over assets without relying on custodial intermediaries

· Privacy protection: safeguarding assets and data through MPC, CryptoNote, and end-to-end encrypted communication

Mixin has been in operation for over 8 years, supporting over 40 blockchains and more than 10,000 assets, with a global user base exceeding 10 million and an on-chain self-custodied asset scale of over $1 billion.

$600 million stolen in 20 days, ushering in the era of AI hackers in the crypto world

Vitalik's 2026 Hong Kong Web3 Summit Speech: Ethereum's Ultimate Vision as the "World Computer" and Future Roadmap

On the same day Aave introduced rsETH, why did Spark decide to exit?

Full Post-Mortem of the KelpDAO Incident: Why Did Aave, Which Was Not Compromised, End Up in Crisis Situation?

After a $290 million DeFi liquidation, is the security promise still there?

ZachXBT's post ignites RAVE nearing zero, what is the truth behind the insider control?