Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Wall Street Flash Mob Run? Mega-Cap Stock Plunge, Goldman's Great Escape, Illustrated Guide to Private Credit Crisis

On Monday, April 6, 2026, the U.S. private credit asset management giant Blue Owl Capital (OWL) saw its stock price drop to $8.45 at the close, hitting a new low since its listing, with an intraday dip to $7.80. The event that triggered this round of selling was the disclosure by Blue Owl the previous Thursday of first-quarter semi-liquid fund redemption data. Its two main illiquid BDCs (Business Development Companies), OTIC (Blue Owl Technology Income) and OCIC (Blue Owl Credit Income), received approximately $5.4 billion in investor redemption requests this quarter, with OTIC seeing a redemption rate of 40.7% of outstanding shares and OCIC at 21.9%. Both funds simultaneously triggered a 5% hard industry gate, only allowing the release of less than $1.2 billion proportionally.

Mainstream financial media immediately framed this as the "Retail Private Credit Narrative Collapse" and "AI Disruption Spillover into Debt Holders." However, these two labels obscured a more critical issue. In the same week, Goldman Sachs Private Credit Corp, under Goldman Sachs Asset Management, had a first-quarter redemption request proportion of 4.999%, just 0.001 percentage points below the 5% gate, making it one of the few, and possibly the only large semi-liquid perpetual BDC that did not trigger the gate, providing full redemption to exiting investors. This redemption wave was not a "private credit collapse" but a clear K-shaped differentiation.

According to Bloomberg's report on April 6, Goldman's $15.7 billion fund was an outlier this quarter in "Dodging Exodus." Meanwhile, Blue Owl's OTIC redemption rate was 8.1 times that of Goldman, and OCIC was 4.4 times. While market attention was entirely focused on Blue Owl's plunge, the real question worth asking is why, with the same structure, the same week, and the same 5% gate, the two institutions presented entirely different outcomes.

Stock Price Evaporates Two-Thirds in Fifteen Months

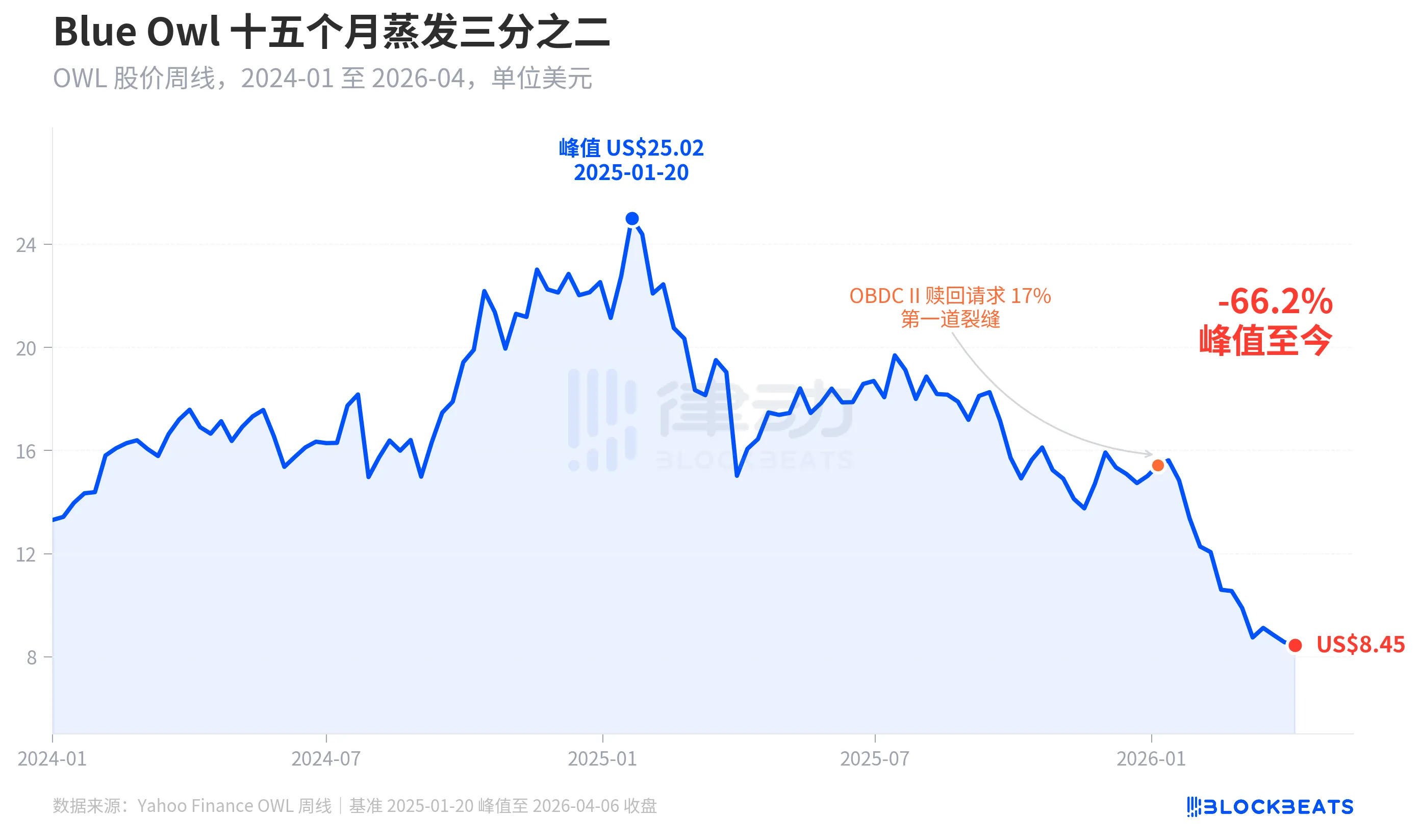

First, let's look at the market's pricing of Blue Owl. According to Yahoo Finance's historical weekly data, Blue Owl Capital (OWL) closed at $25.02 on January 20, 2025, marking its all-time high. By the week of April 6, 2026, it closed at $8.45, plummeting by 66.2% over fifteen months, evaporating nearly two-thirds of its market value.

The first significant crack in the stock price appeared in early January 2026 when another fund under Blue Owl, OBDC II (a smaller private BDC), disclosed receiving redemption requests equivalent to 17% of outstanding shares, seen as the "first crack." Subsequently, the stock price declined steadily until the end of the first quarter, when both OTIC and OCIC, two flagship funds, simultaneously triggered gates, with the intraday price touching a record low of $7.80 since the IPO.

Interestingly, the decline in Blue Owl's stock price (-66.2%) far exceeded the degree of its fundamental deterioration. OCIC still holds $36 billion in AUM, with a first-quarter 2026 NAV decline of approximately 6.5%, and the company's total AUM remains above $290 billion. The market appears to be repricing the company based on factors such as "uncertainty of future redemptions" and "confidence erosion in valuations," rather than solely on current performance.

Same Gate, Different Destinies

What truly illustrates "K-shaped divergence" is the cross-section. When five large semi-liquid perpetual BDCs that publicly disclosed redemption data in the first quarter of 2026 are compared, the structural differences become clear.

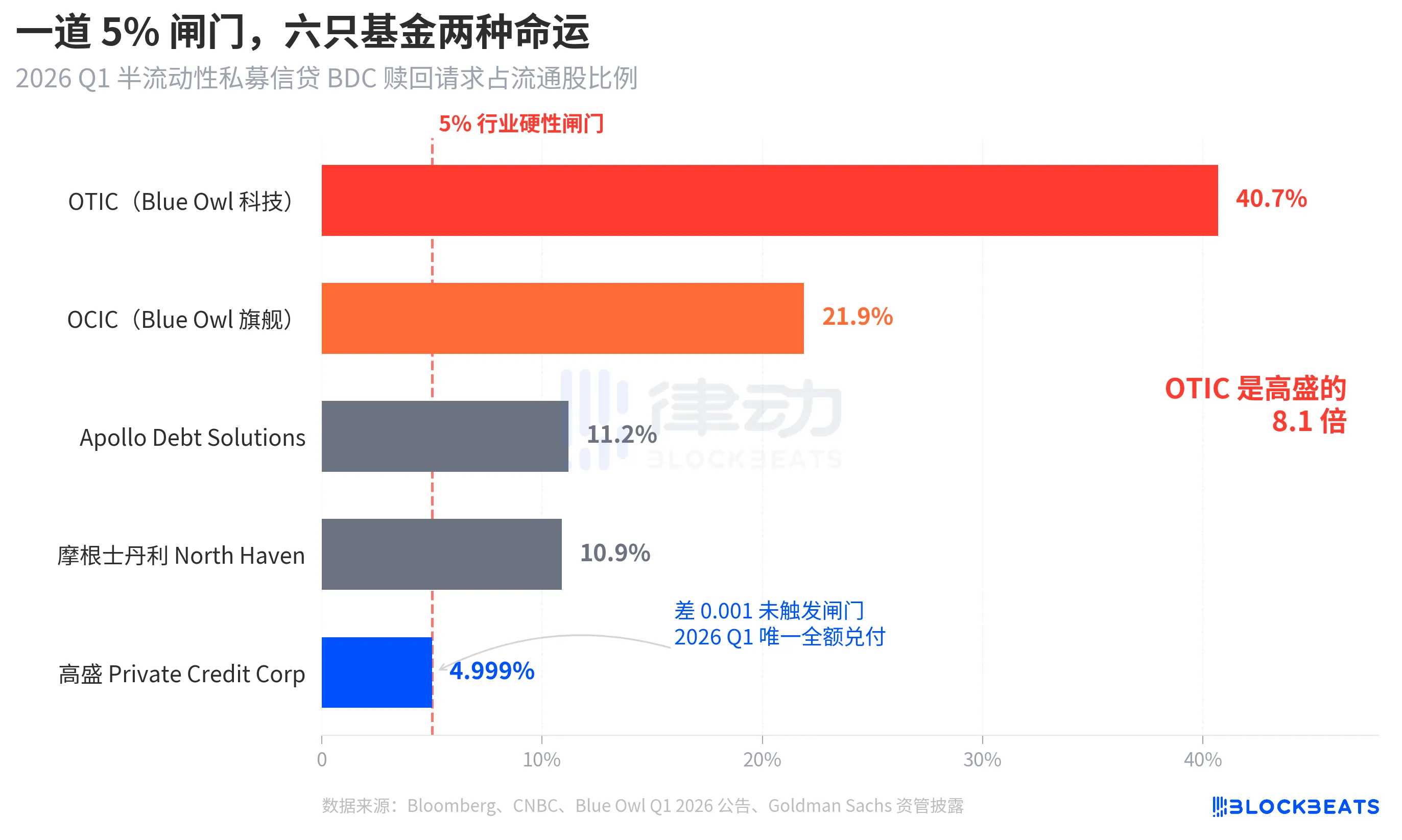

According to Bloomberg, CNBC, and each fund's corporate announcements, the redemption rates of the five funds are as follows: Blue Owl OTIC 40.7%, Blue Owl OCIC 21.9%, Apollo Debt Solutions 11.2%, Morgan Stanley North Haven Private Income Fund 10.9%, Goldman Sachs Private Credit Corp 4.999%. These five funds can roughly be divided into three tiers.

In the top tier, both Blue Owl funds significantly exceeded the gate, with almost half of OTIC's shareholders looking to withdraw and OCIC nearly four times the gate. Following the rule to only allow redemptions of up to 5% of outstanding shares, OTIC actually redeemed approximately $179 million, while OCIC redeemed around $988 million, locking out over $4.2 billion in excess redemption requests beyond the gate.

In the middle tier, both Apollo and Morgan Stanley have redemption rates ranging from 10% to 11%. According to Bloomberg reports on March 11 and March 23, Apollo Debt Solutions redeemed about 45% of requests, North Haven redeemed about 46%, also triggering gates but with significantly less pressure compared to Blue Owl.

Undergate, only Goldman Sachs. 4.999% is the only large fund that did not trigger the 5% gate at the same time, with all redemption requests being fully redeemed.

Bloomberg used "Dodges Exodus" in the article title, with OTIC being Goldman Sachs' 8.1x this figure, which in itself indicates the intensity of differentiation. In the same week, with the same structure, under the same rules, the fate of the two institutions is completely different.

Bubble, Retail Investors Drive It Up 4.4x

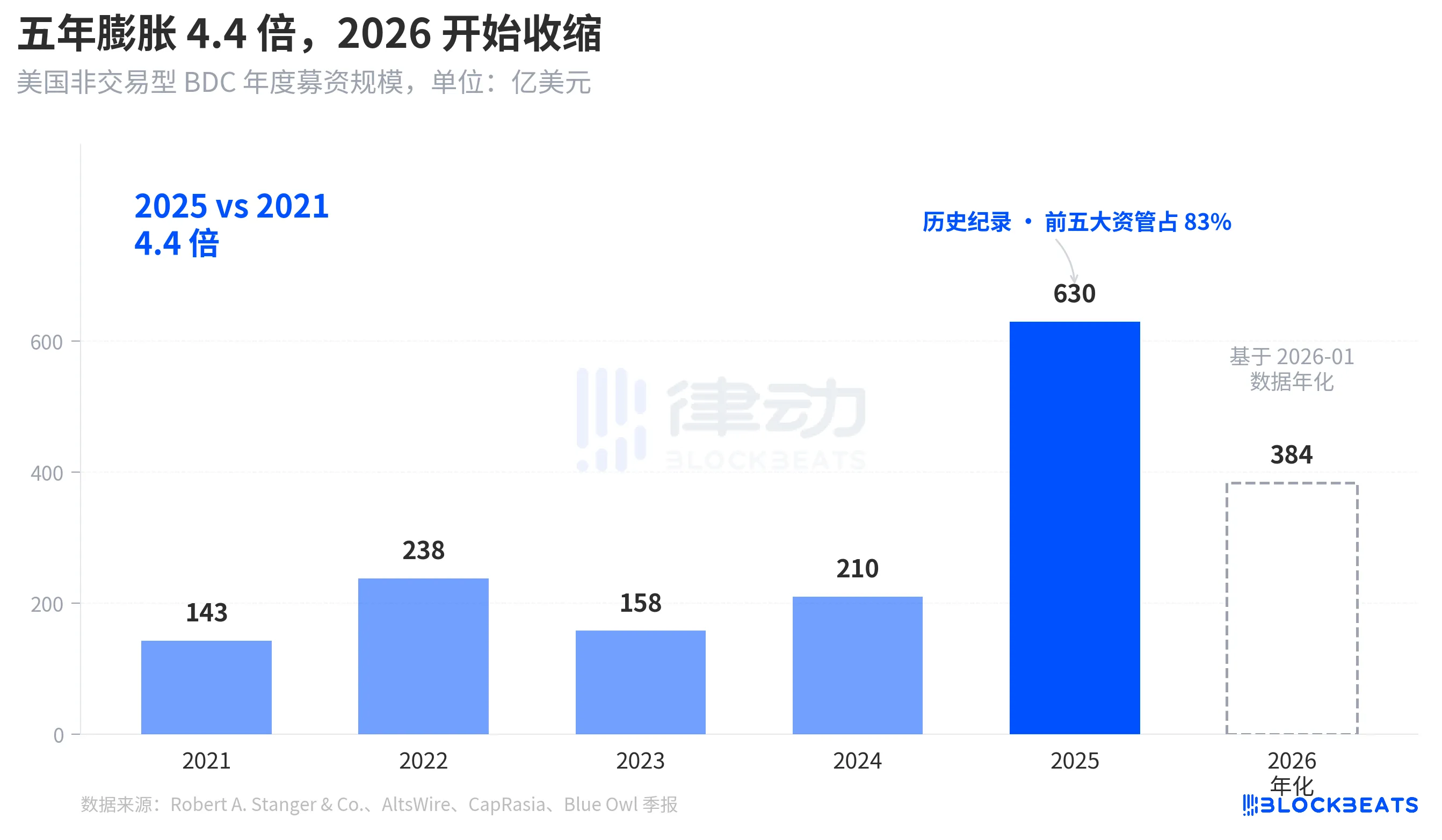

To understand why this redemption wave came so fiercely, you first need to see how deep the incoming water is. According to industry statistics from Robert A. Stanger & Co., the annual fundraising scale of U.S. non-traded BDCs over the past five years has shown a clear parabolic trend.

From $14.3 billion for the full year 2021 to a historical record of $63 billion for the full year 2025, a 4.4x increase over five years. The same statistics show that the top five institutions (Blackstone, Blue Owl, Apollo, Ares, and HPS) took about 83% of this, around $52.3 billion flowing into the top five. The retail funds that poured in over the past five years were not only enormous in total amount but also extremely concentrated in distribution.

However, as of January 2026, Stanger's monthly data shows that non-traded BDC fundraising was only $3.2 billion, nearly half of the peak of $6.2 billion in March 2025. According to reports from Connect Money and FinancialContent, BDC overall sales in the first quarter of 2026 decreased by about 40% compared to the same period last year. In the same quarter when investors began concentrating redemption requests, new inflows visibly decelerated. The simultaneous rise in redemption pressure and decline in new purchases caused the gate to be slammed harder than anyone had expected.

This is not a cyclical retracement but a narrative shift, with BDCs as a semi-liquid perpetual "savings-like product" sold to retail investors being reexamined at the fund level for the first time.

From BREIT to Blue Owl, Vulnerability Becomes Evident Over Four Years

Placing this redemption wave on a longer timeline reveals that it did not erupt suddenly.

The structure of "semi-liquid perpetual" has two layers of commitment. It allows funds to remain unlisted, with no public valuation, while promising investors to redeem a portion of shares quarterly based on NAV. Essentially, this packages illiquid assets (private credit, private real estate) into a product that "seemingly allows for immediate withdrawal." To prevent a run, the industry uniformly set a 5% quarterly redemption gate, where once redemption requests exceed 5% of outstanding shares, the fund redeems proportionally, and the remaining requests are locked up until the next quarter.

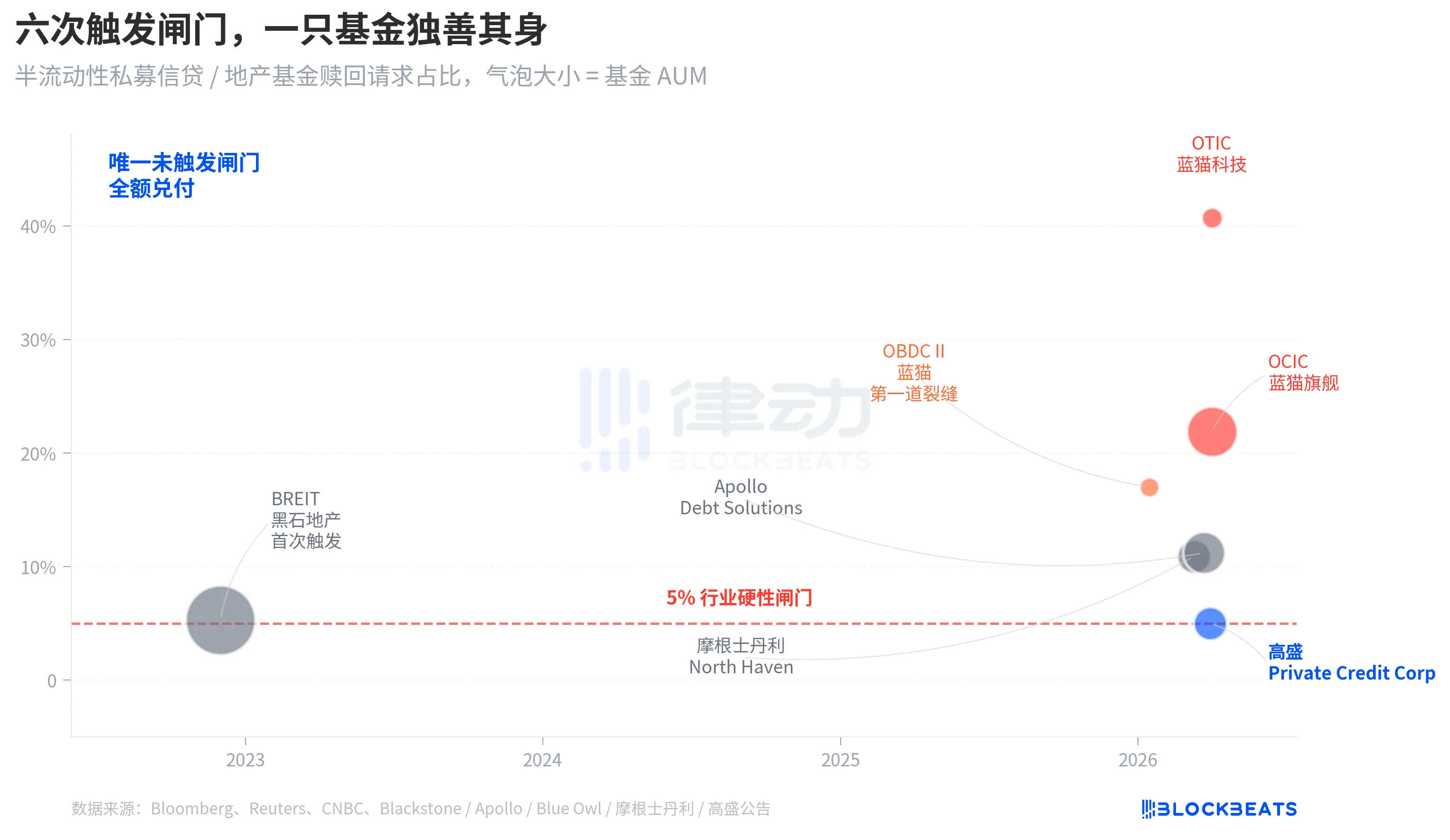

In November 2022, Blackstone's non-traded real estate investment trust BREIT triggered this gate for the first time, becoming the inaugural systematic liquidity event of a perpetual semi-liquid structure. According to Caproasia data, in January 2023, BREIT only honored 25% of redemption requests for the month, totaling $14.3 billion in redemptions by November 2023. Seen as an isolated event within the real estate asset class, the private credit market was not dragged down.

Four years later, the same fault line that had spread through real estate reached credit. In January 2026, Blue Owl OBDC II disclosed a 17% redemption request, serving as the first signal. On March 11, Morgan Stanley North Haven triggered the gate. On March 23, Apollo Debt Solutions triggered the gate. On April 2, both Blue Owl OCIC and OTIC simultaneously triggered the gate. Within seven days, four top asset-managed large BDCs were consecutively caught in the same threshold, while Goldman Sachs remained outside the gate that quarter with a 4.999% margin.

The structural fragility of the semi-liquid perpetual BDC was not exposed by Blue Owl's redemption surge; it had been on the table since BREIT's 2022 event, but no one had truly taken it seriously in four years.

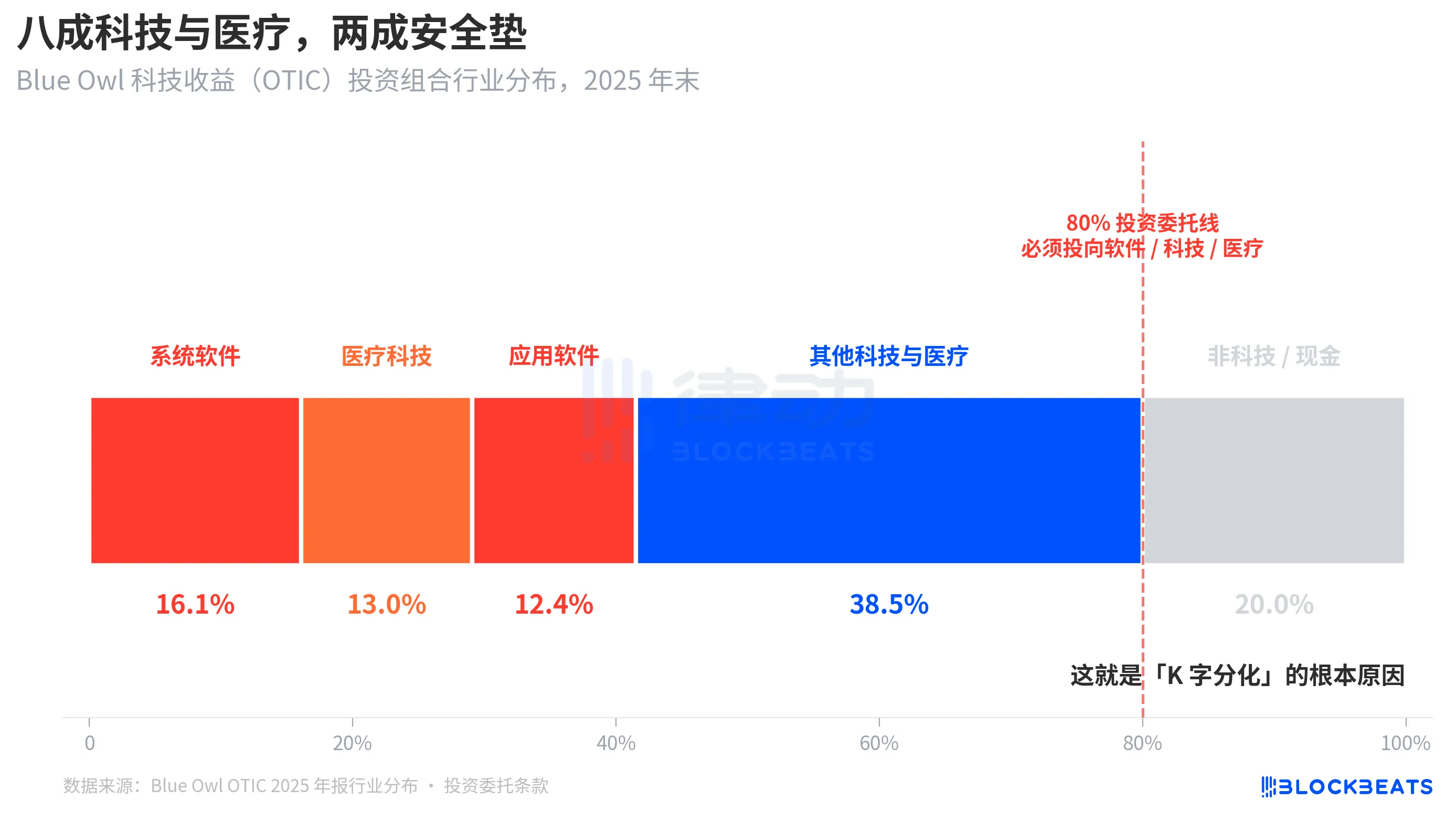

Root Cause: 80% of OTIC Exposure in Tech and Healthcare

Now back to that critical question: Why did Goldman Sachs and Blue Owl have such divergent outcomes with the same structure in the same week? Disaggregating OTIC's portfolio provides a clear answer.

According to a KBRA rating report and Blue Owl OTIC's Q4 2024 financials, as of the end of 2025, OTIC's portfolio size was $6.2 billion, holding stakes in 190 companies across 39 end markets, with 92% backed by private equity funds and 93% being first-lien senior secured loans. On paper, this is a fundamentally sound fund, but its industry concentration is quite unique. System software accounts for 16.1%, medical technology for 13.0%, and application software for 12.4%, totaling 41.5% in just these three subsectors.

The key point is that this is not a temporary industry preference of the manager, but a hard rule written into the OTIC investment charter, requiring at least 80% of total assets to be invested in "software and tech-related" companies. Blue Owl describes OTIC in its public materials as primarily investing in large, market-leading software companies that provide mission-critical, recurring revenue solutions. OTIC was designed from the outset to be a SaaS technology credit fund.

Within the market narrative of the past six months, SaaS has been one of the asset classes most severely repriced by AI. When investors began to worry about the "AI disruption of long-term subscription revenue for software companies," a private credit fund with an 80% exposure to software and technology was particularly affected. According to Bloomberg and Reuters, Blue Owl's management themselves acknowledged in their communications to investors that part of the first-quarter redemption pressure came from "AI disrupting software companies."

In contrast, the investment portfolio of Goldman Sachs Private Credit Corp (with $15.7 billion AUM) was described by Bloomberg as "significantly more diversified than its peers," with no single industry exposure reaching OTIC's level of tech exposure. Similar private credit, similar semi-liquid structure, similar 5% gate, but one had an exposure of over 80% to the current market theme while the other had less than 15%, resulting in a redemption rate of 40.7% for one and 4.999% for the other.

This is the fundamental reason for the "K-shaped differentimentation." It's not that private credit as an asset class collapsed, but rather that funds concentrated on the same market theme ran into trouble, while diversified funds were hardly affected. The differentiation occurred at the risk exposure level, not at the structural level.

Wrap-Up

JPMorgan CEO Jamie Dimon, in the shareholder letter for 2026 released on April 6, happened to coincide with the day Blue Owl hit a new low. In the letter, he wrote: Private credit, in general, lacks transparency and strict loan valuation markings, which makes people more likely to sell if they think the environment will worsen, even if the actual losses have hardly changed.

Dimon's statement points to a structural issue. Private credit is difficult to mark-to-market, and holders' perception of risk is more sensitive than actual losses. Reading this on April 7, 2026, has two meanings. One is that 0.001% difference at Goldman Sachs was more a result of a diversified structure than luck. The other is that the entire $1.8 trillion private credit market has yet to resolve the underlying contradiction of "liquidity versus opaque portfolio."

A 5% threshold failed to split Blue Owl and Goldman Sachs into a "good fund" and a "bad fund"; it simply settled two different investment decisions — "concentrated bet on current theme" and "diversification" — in a single candlestick.

You may also like

The 17-Year Mystery Will Be Solved, Who is Satoshi Nakamoto?

5 Minutes to Make AI Your Second Brain

Uniswap is trapped in an innovation dilemma

What is the key to competition in crypto banking?

The flow of stablecoins and the spillover effects in the foreign exchange market

After two years, Hong Kong's first batch of stablecoin licenses finally issued: HSBC, Standard Chartered make the cut

The person who helped TAO rise by 90% has now single-handedly crashed the price again today

3-Minute Guide to Participating in the SpaceX IPO on Bitget

Top 5 Cryptos to Buy in 2026 Q1: A ChatGPT Deep Dive Analysis

Explore the top 5 cryptos to buy in Q1 2026 including BTC, ETH, SOL, TAO, and ONDO. See price outlooks, key narratives, and institutional catalysts shaping the next market move.

How to Earn $15,000 with Idle USDT Before Altcoin Season 2026

Wondering if altcoin season is coming in 2026? Get the latest market update, and learn how to turn your idle stablecoins waiting for entry into extra rewards up to 15,000 USDT.

Can You Win Joker Returns Without Large Trading Volume? 5 Mistakes New Players Make In WEEX Joker Returns Season 2

Can small traders win WEEX Joker Returns 2026 without huge volume? Yes—if you avoid these 5 costly mistakes. Learn how to maximize card draws, use Jokers wisely, and turn small deposits into 15,000 USDT rewards.

Altcoin Season 2026: 4 Stages to Profit (Before the Crowd FOMO In)

Altcoin Season 2026 is starting — discover the 4 key stages of capital rotation (from ETH to PEPE) and how to position before the peak. Learn which tokens will lead each phase and avoid missing the rally.

Will Alt season come in 2026? 5 Tips to Spot the Next 100x Crypto Opportunities

Will altcoin season arrive in 2026? Discover 5 rotation stages, early signals smart traders watch, and the key crypto sectors where the next 100x altcoin opportunities may emerge.

The bear market has arrived, and cryptocurrency ETF issuers are also getting involved

The richest man had a quarrel with his former boss

BTC Firm Above 70K! Saylor’s "Institutional Logic" vs. Moon’s "Retail Faith": Who is Really Harvesting the Market?

Bitcoin is holding firm above the $70,000 support level following a massive short squeeze that liquidated $427 million. As the "Four-Year Cycle" narrative shifts, the market is split: Michael Saylor’s cold, institutional "indiscriminate stacking" vs. Carl Moon’s high-energy retail "hopium." This article decodes these two polar-opposite strategies for the 2026 bull run and reveals how WEEX’s institutional-grade liquidity and AI trading tools empower every type of investor to convert market volatility into profit.

The Girl Who Created the SBTI Test: A Story of a Doomed Cyber Love, an E-Widow Ratfolk