Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Why Should I Short SOL?

Original Author: The Giver

Original Translation: Ismay, BlockBeats

Editor's Note: This article provides an in-depth analysis of Solana's recent performance, discussing potential challenges from supply events, competitive pressures, complacency, among other perspectives, and predicts the future market trend. The author, through data and market phenomena, reveals Solana's potential concerns in terms of fund flows, ecosystem competition, and investor behavior, while also highlighting the changing trend of marginal buying and selling pressure in the market.

The following is the original content:

Here are some brief thoughts on Solana, mainly discussing why I believe Solana may underperform compared to other assets in December (I believe this trend has already started but will continue).

I opened a short position around ~$235-240 and believe this is the last excellent asymmetric opportunity of the year. However, it should be noted that I also hold short positions on other assets (such as Bitcoin, as the price gap between Saylor's buy-in price and the ETF is widening; also, I think if Ethereum falls, its downward trend may last even longer).

In summary, most of Solana's performance this year has not truly been tested, and its main driving force is running out (or in the process of running out).

Why will SOL underperform?

In my view, the real factors that have driven Solana to become the best-performing asset in the YTD among scalable assets this year include the following:

1. A more active and diversified ecosystem than its competitors, with fast transaction speeds;

2. The most powerful "casino" environment that has attracted many meme participants willing to use SOL as a unit of account;

3. Mid-year inflows — I believe many fund managers and large liquidity participants have been squeezed out due to the lack of ETH ETF heat, experiencing some form of "existence crisis" in future asset allocation.

Today, I believe the above three main driving forces have weakened and are highly vulnerable to shocks, with a significant amount of excess froth still needing to be trimmed. Here are my specific reasons:

As a speed- and diversity-focused leading L1, Solana faces a strong threat from HYPE and ETH/Base

The rise of these threats has been unexpected and remains inadequately addressed.

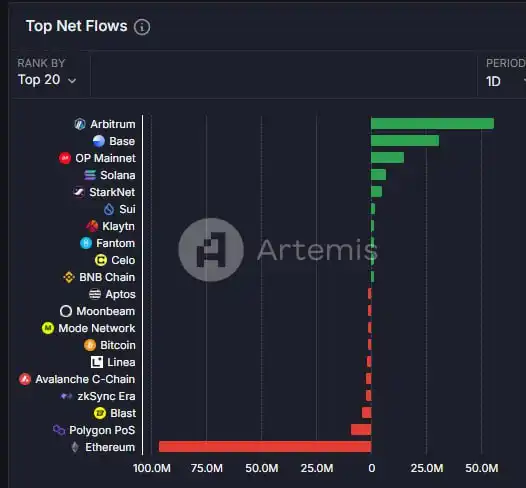

The chart below shows Artemis traffic data, where you can choose to view it over a 1-week or 1-month period. This is the most significant instance this year of Solana's capital flow shifting to EVM, a shift that is reflected not only in traffic. We can also observe this in popular domain use cases, such as the meme coin sector in the AI domain—previously considered top-tier projects like GOAT, FARTCOIN, ZEREBRO, and AI16Z have all halved in valuation during this period, while the VIRTUAL and proxy ecosystems have flourished.

Furthermore, I believe Solana has not faced a true competitor in the L1 space for quite some time. While the HYPE is still in its early stages, its pursuit of democratizing ownership and the team's demonstrated strength are attractions that cannot be ignored in the short term.

Solana has yet to experience a true supply shock event by 2024

In contrast, other major assets have already undergone severe tests, such as Bitcoin's MTGOX incident and regulatory issues in Germany, as well as Ethereum's ETF launch. Solana has almost been unaffected in this regard, with only a brief fluctuation during the Jump sell-off earlier this summer, quickly brushed aside as ETH's larger retracement diverted attention.

The period of the last few months has been Solana's time to shine as a high beta asset to Bitcoin, capturing much of the capital flow from Ethereum (a trend that has gradually dissipated) while attracting attention far beyond lackluster, unappealing small-cap altcoins.

In the realm of liquid funds, for the 2024 fiscal year, GPs should have only two options for realizing cash distributions:

1. Distribute based on a percentage of realized gains;

2. Distribute based on a percentage of unrealized gains but subject to clawback adjustment based on the prior year's high watermark.

In either case, given Solana's outstanding performance last year, I believe fund managers would lean toward selling SOL, reasons for which may include:

a) As the best-performing asset of the year, it has seen a significant price increase;

b) It is believed that parts of the portfolio that have previously underperformed still have untapped upside potential and are more worthy of holding, while also observing other altcoins that have shown trend strength recently on the H1/H4/1 timeframes to capture gains.

Furthermore, this trend is also being driven by the hype around the Galaxy Auction (SOL cost basis at $80-100). Fund managers participating in the auction can profit in the following ways:

For example, selling one-third of the locked supply purchased near historical highs and then "reclaiming" these tokens in the first unlock event in March of next year to realize the price difference in nominal value.

The exit liquidity of the SOL ETF weakened due to the rise of established tokens and the potential impact of the XRP ETF

XRP's performance is being driven by two main factors:

a) It is considered the asset most likely to launch an ETF product after ETH, closely linked with Bitwise;

b) Rumors of the U.S. cryptocurrency capital gains tax dropping to 0%.

Considering XRP's track record (as one of the earliest crypto assets) and SEC Chair Gary Gensler's resignation, even if the probability of an XRP ETF launch remains on par with or slightly lower than SOL, it is undeniable that it is diverting market share that originally belonged entirely to SOL.

Complacency

Although this sentiment is difficult to quantify precisely, intuitively, I believe Solana's arrogance has reached a bottleneck, contrasting the situation from a few years ago — back then, ETH caught up with SOL head-on due to its superior position, and that position acted as an impenetrable moat.

Here are some typical examples:

1. "Network Expansion vs. L2"; DRIFT compared to HL, demonstrating an "incorruptible" attitude;

2. Many claim "no one would ever want to bridge from Solana to Base," despite clear counterexamples;

3. Some users who were staunch supporters of ETH surrendered completely a few weeks before ETH's 35% surge, with some suddenly strongly predicting that the target price for ETHSOL would plummet to very low levels (e.g., 0.027 ETHSOL).

Summary

In the next 30 days, I believe the attractiveness of Solana to marginal buyers is at its weakest point this year (ETF liquidity significantly lags behind ETH; the attention on altcoins is more diversified than before), while the selling pressure from marginal sellers is at its strongest (profit-taking; users who have made significant gains through memes or holding SOL choosing to sell to cash out and hedge).

Furthermore, as the bulls attempt to drive the price up, the funding cost remains high, with this upward movement being entirely leveraged-driven and reflected in recent (yet short-lived) ATH breaches.

You may also like

The 17-Year Mystery Will Be Solved, Who is Satoshi Nakamoto?

5 Minutes to Make AI Your Second Brain

Uniswap is trapped in an innovation dilemma

What is the key to competition in crypto banking?

The flow of stablecoins and the spillover effects in the foreign exchange market

After two years, Hong Kong's first batch of stablecoin licenses finally issued: HSBC, Standard Chartered make the cut

The person who helped TAO rise by 90% has now single-handedly crashed the price again today

3-Minute Guide to Participating in the SpaceX IPO on Bitget

Top 5 Cryptos to Buy in 2026 Q1: A ChatGPT Deep Dive Analysis

Explore the top 5 cryptos to buy in Q1 2026 including BTC, ETH, SOL, TAO, and ONDO. See price outlooks, key narratives, and institutional catalysts shaping the next market move.

How to Earn $15,000 with Idle USDT Before Altcoin Season 2026

Wondering if altcoin season is coming in 2026? Get the latest market update, and learn how to turn your idle stablecoins waiting for entry into extra rewards up to 15,000 USDT.

Can You Win Joker Returns Without Large Trading Volume? 5 Mistakes New Players Make In WEEX Joker Returns Season 2

Can small traders win WEEX Joker Returns 2026 without huge volume? Yes—if you avoid these 5 costly mistakes. Learn how to maximize card draws, use Jokers wisely, and turn small deposits into 15,000 USDT rewards.

Altcoin Season 2026: 4 Stages to Profit (Before the Crowd FOMO In)

Altcoin Season 2026 is starting — discover the 4 key stages of capital rotation (from ETH to PEPE) and how to position before the peak. Learn which tokens will lead each phase and avoid missing the rally.

Will Alt season come in 2026? 5 Tips to Spot the Next 100x Crypto Opportunities

Will altcoin season arrive in 2026? Discover 5 rotation stages, early signals smart traders watch, and the key crypto sectors where the next 100x altcoin opportunities may emerge.

The bear market has arrived, and cryptocurrency ETF issuers are also getting involved

The richest man had a quarrel with his former boss

BTC Firm Above 70K! Saylor’s "Institutional Logic" vs. Moon’s "Retail Faith": Who is Really Harvesting the Market?

Bitcoin is holding firm above the $70,000 support level following a massive short squeeze that liquidated $427 million. As the "Four-Year Cycle" narrative shifts, the market is split: Michael Saylor’s cold, institutional "indiscriminate stacking" vs. Carl Moon’s high-energy retail "hopium." This article decodes these two polar-opposite strategies for the 2026 bull run and reveals how WEEX’s institutional-grade liquidity and AI trading tools empower every type of investor to convert market volatility into profit.

The Girl Who Created the SBTI Test: A Story of a Doomed Cyber Love, an E-Widow Ratfolk